If you bought your Spanish holiday home with renting it out on Airbnb in mind, getting insights on what the return on investment is, is crucial. At least, that's what we think. For us, the penthouse we bought is an investment first and a nice place for ourselves second. So I want to know what the property is generating in profits.

These are the 3 things I keep an eye on to get my ROI:

1) Free cash flow generated by the property

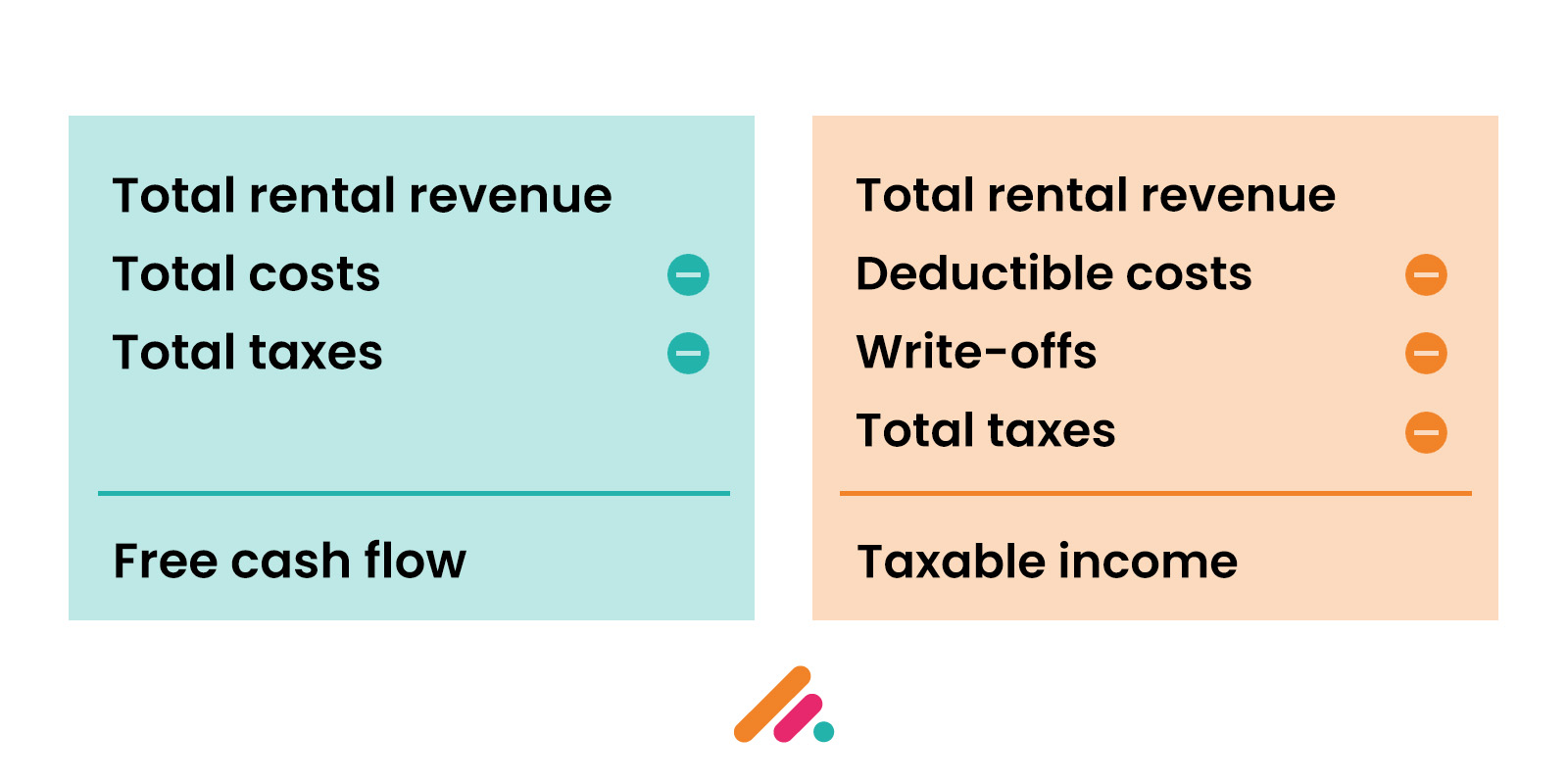

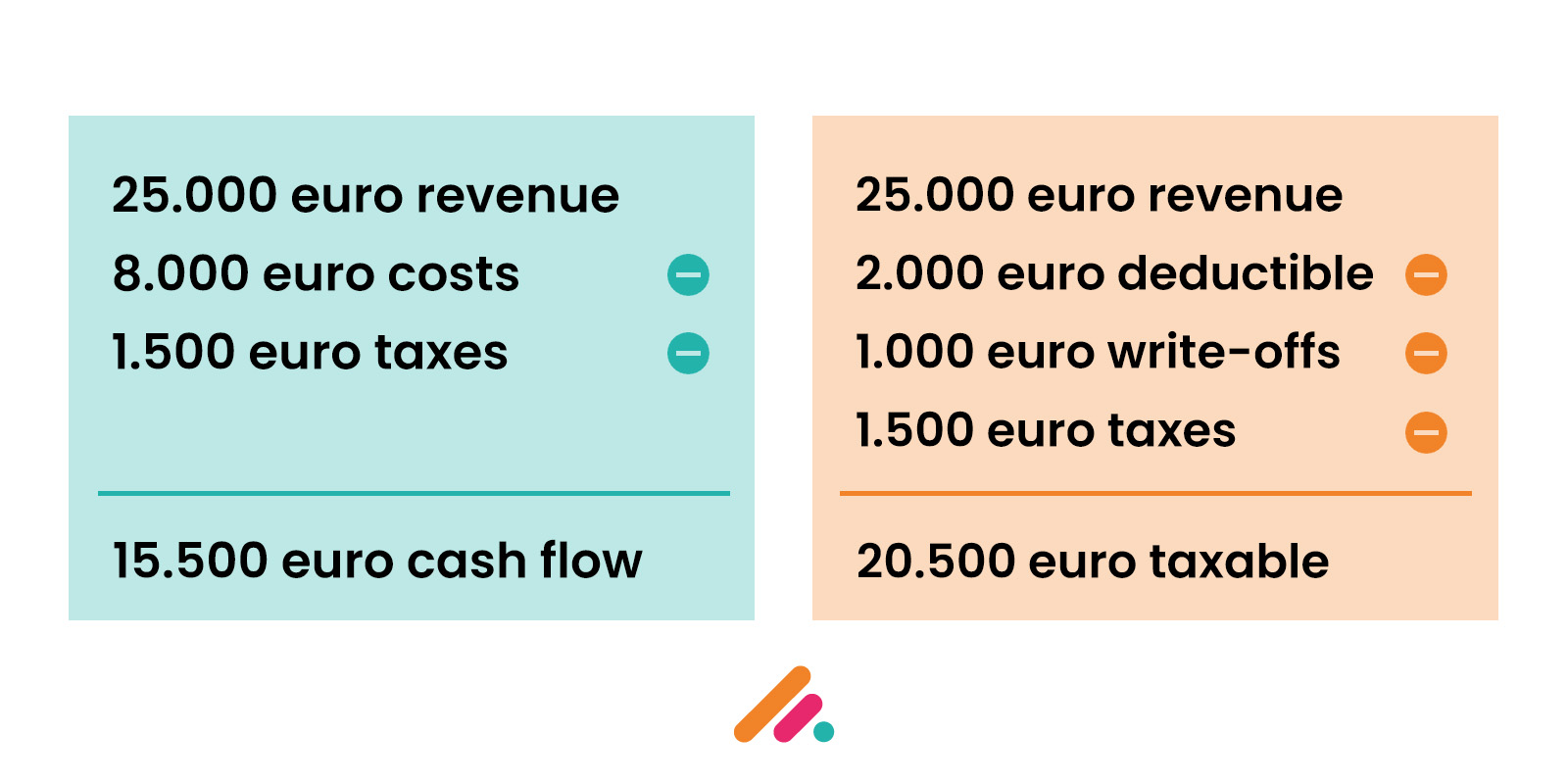

Free cashflow is my main indicator of how my Spanish airbnb is performing financially. I'm choosing the free cash flow over the taxable income, because the free cashflow is the actually money in the bank.

Here are some differences between the two, by using an example:

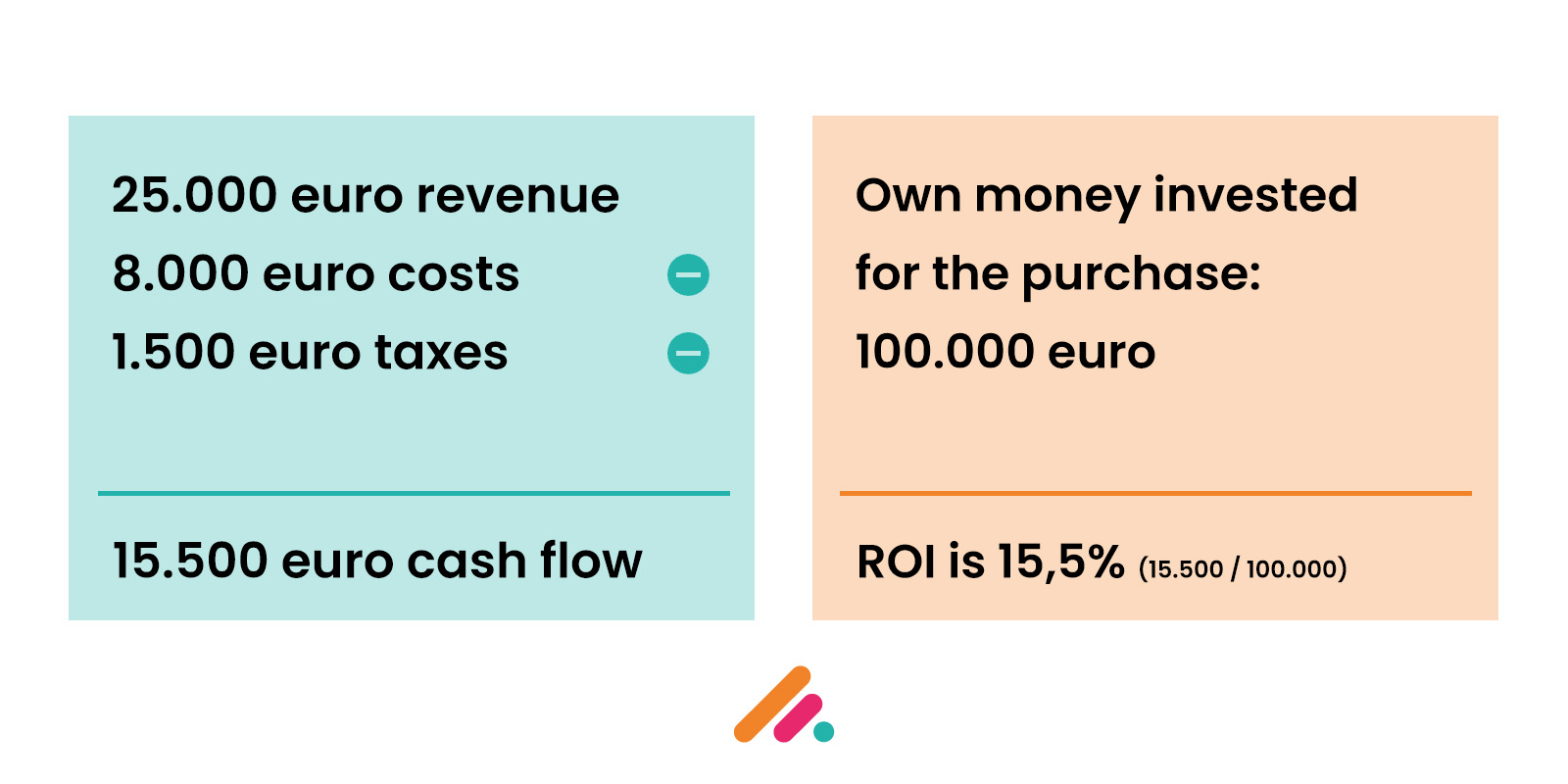

You'll see that the taxable income is higher than the actual free cash flow. That is because not all costs are 100% deductible for taxes. For example, furniture you purchased can be written off 10% per year, while obviously the money out of pocket is 100%.

Free cash flow is money in the bank. I'd always use that to determine ROI. It's reality vs. paper ;-)

In case you have a mortgage on your property, don't forget to include the full payment in the costs for your cash flow calculation!

2) Financial investment made on purchase

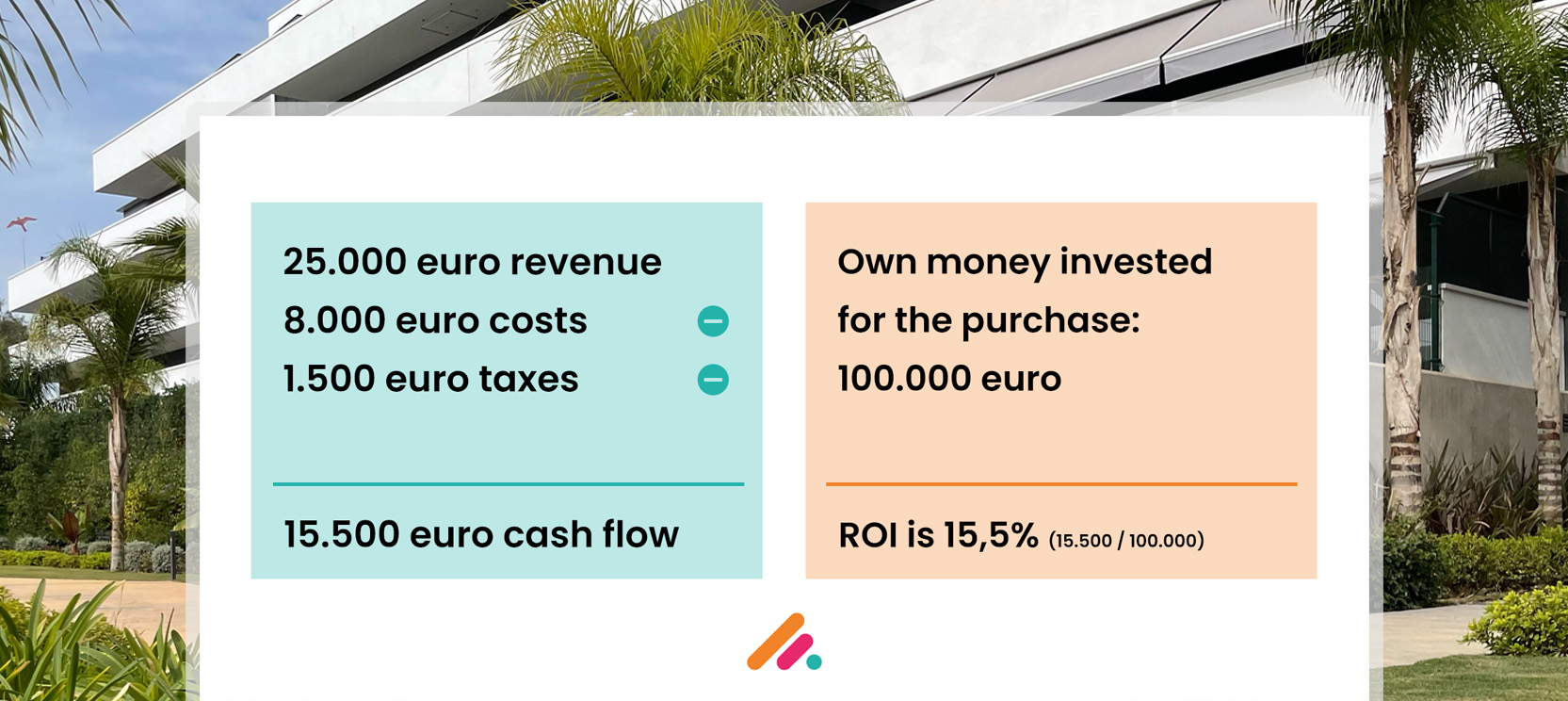

When you bought your property in Spain, you were required to put in some money of your own. Probably 30%-40% or so. Let's say for the sake of an easy calculation that I bought my property for 300.000 euro, and I had to fork out 100.000 euro of my own money for the purchase. The other 200.000 euro I used a mortgage for.

The 100.000 euro of my own money is my own financial investment. This is the amount I'd like to calculate the ROI on.

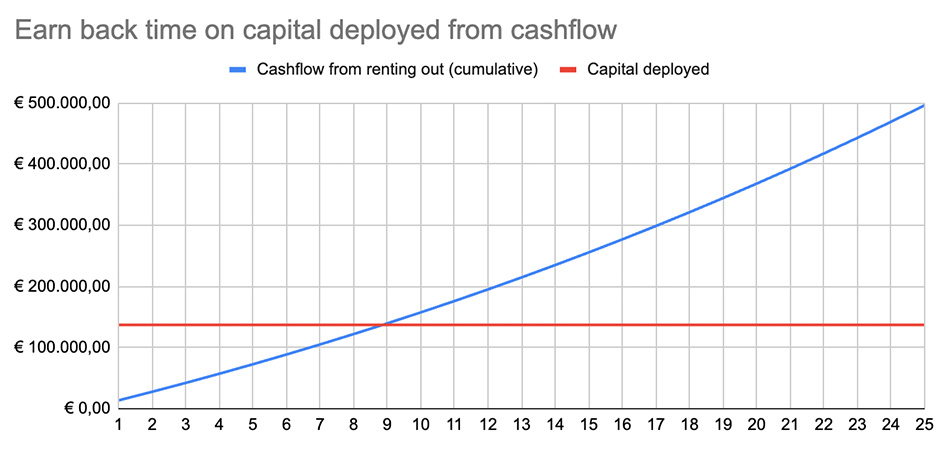

In the example above, the annual ROI is 15.500 euro on an investment of 100.000 euro. So, that makes 15,5% ROI. And, this is without taking into account the appreciation of the property value.

If you'd have this 15,5% ROI every year, than you'd earn back your investment in about 6,5 years. Which is pretty fast!! You could buy another property then and multiply your cash flow.

3) Property valuation of the evolution of it

The value of the property is not cash money in the bank. It's paper value that only hits your bank account when you sell. However, what I like to do is use the property value as an indicator of the "health" of my property. For me, this is more a long term thing. I keep track of the cash flow the property generates every year and in the end add that cash flow to the property valuation.

In my example, I used a property value of 300.000 euro, of which 100.000 euro was paid with own money. Say, after 5 years, the property is worth 400.000 euro (not unrealistic in these days). That would give you 200.000 euro value over your mortgage (also 200k). So, you're up 200k on the mortgage (and if you count in your invested money you're up 100k).

I use the property value to get a total overview of ROI and value of the property. I plan to add properties to my portfolio in the future and this total overview will help me build that portfolio easier.